Investors have witnessed higher-than-usual volatility in the public equity market over the last several weeks, largely in response to the series of tariff announcements and subsequent economic uncertainty over global trade policy that is unfolding. Equity prices are swinging daily on headlines related to the pace and impact of potential tariffs that may roil the U.S. and the global economy. Investors have a very current, albeit sometimes agonizing, window into the valuation of their public equity holdings due to the transparency of the public trading system. But what about the valuation of private company investments made by private equity fund managers and their limited partners? How does the recent volatility impact those investments, which are often described as “patient capital” due to their longer-term and less liquid structures?

While changes to public company stock prices can be observed minute-to-minute and may sometimes lead to indiscriminate selling, volatility impacts privately held company valuations in an indirect, lagged, and often less severe fashion. It is important to note that private companies are valued in three main ways: 1) forecasting future cash flow generation and discounting those aggregate flows back to a present value; 2) comparing a business to public companies in the same industry sector; and/or 3) looking at precedent transactions (i.e., what prices did buyers and sellers negotiate for similar assets in recent months). As public stock prices fall, the enterprise value multiples of those companies decline, at least temporarily. Eventually such reductions in enterprise value may similarly affect the valuation of a comparable private company. However, private equity valuations are updated at most on a quarterly basis and sometimes only annually. Therefore, any meaningful change in public equity prices impacts private companies on a three-to-six-month lag and may be muted by idiosyncratic strength in business fundamentals and free cash flow.

One risk dimension facing the private market ecosystem today is its ability to assess tariff exposure across existing portfolios, which often comprise companies in different industries. In much the same way that certain sectors in public markets have been more impacted by tariff news (and implementation), not all private companies will be affected equally. Profitable, cash-flow-positive companies will likely hold value better. And sector matters, with retail, auto, technology, and home construction facing more significant supply chain challenges than others (with some exceptions, of course). Really, any business that relies on a deeply integrated supply chain and/or key imports may be negatively impacted. A new premium will be placed on tariff management skills and insight into impacted end markets, supply chains, and foreign exposure across private equity portfolios.

An additional consideration is the impact of volatility on the dealmaking environment in which private equity purchases and exits occur. Prior to “Liberation Day,” there was optimism that the Administration’s new tariff plan would bring much-needed clarity, encouraging private equity fund managers to move forward with transactions. However, the announced plan proved far more severe than anticipated. With rising recession fears, retaliatory tariffs, and increasing concerns over inflation and interest rates, many managers are now more cautious about deploying fresh capital.

Furthermore, these market dynamics may stall an already sluggish private markets exit environment. One key exit strategy — taking a portfolio company public — has become increasingly difficult in the face of elevated stock market volatility. Fluctuating valuations and unpredictable investor sentiment have made IPOs more challenging to execute. Despite a promising uptick in IPO filings during the first quarter and several successful launches, many companies are reassessing or delaying their plans, opting to wait for more stable conditions.

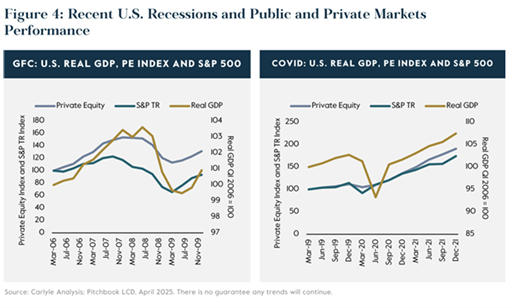

However, private equity investors should remain reasonably optimistic about their funds’ ability to weather this tumult. Private equity investment periods can span up to a decade to enable fund managers to implement operational improvements and accretive acquisitions, as well as to time their exit just right, hence the term “patient capital”. This longer-term view may provide relative stability during volatile public markets. As noted in a recent Carlyle Group newsletter (“The Carlyle Compass” April 22, 2025), “while today’s protectionism-driven market conditions may lead to different outcomes, the values of private equity-backed companies showed relative resilience during recent periods of recession”. During both the Great Financial Crisis and the COVID pandemic, the Preqin Private Equity index declined far less than the S&P (see chart below).

Ultimately, what matters to the success of a private investment is if the private equity fund manager valued the company appropriately when the investment was made, implemented operational improvements to grow revenue and margins over time, and sold at a meaningful premium to the entry point. Interim fluctuations in value stemming from public market cycles and tantrums are ultimately less important than the company’s ability to successfully execute its business plan and meet its forecasted financial performance. As investors, we should remember that patience is, indeed, a virtue in life…and in private markets.