Dear HCA Clients and Friends,

There has certainly been no shortage of news coverage and analysis over the last several months as the widely anticipated legislation known as the One Big Beautiful Bill Act (OBBBA) made its way through Congress and was signed into law on July 4, 2025. Yet, at the same time, it has been difficult to assess the full scope and impact of the bill as it morphed throughout its passage, with implementation details and timing remaining fluid even today. What follows is a brief summary of tax provisions within OBBBA that may interest our clients.

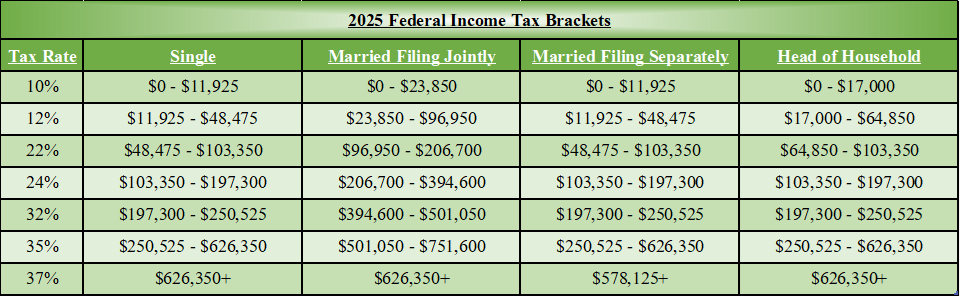

One principal result of the tax portion of the bill was to make permanent (for now) many of the tax provisions of the 2017 Tax Cut and Jobs Act (TCJA) that were scheduled to sunset at the end of this year. Among the provisions that will remain are the current tax brackets, with a top bracket of 37% (see chart that follows this message); the enlarged standard deduction and limitations on itemized deductions that have simplified tax reporting for many; the limit on mortgage interest deduction to the first $750,000 of home acquisition debt; the section 199A 20% deduction for qualified business income (QBI); and the child tax credit, which rises to $2,200 per child for 2025. The estate and gift tax exemption, which is currently $13.99 million per person but was scheduled to be cut in half in 2026 has instead been made permanent at $15 million per person ($30 million per married couple), indexed to inflation, beginning in 2026.

The OBBBA does introduce some new provisions and significant tweaks to existing provisions. Among these are:

- Increase in the SALT cap beginning in 2025. The TCJA capped deductions for state and local taxes at $10,000. Through tax year 2029, OBBBA raises the cap to $40,000 for joint filers ($20,000 for married filing singly), subject to a phasedown as income increases and bottoming out at $10,000 for those with AGI over $600,000. The pass-through entity workaround (PTET) is still available for those who have a pass-through business entity that can pay those taxes. This increase will revert to the original $10,000 level in 2030.

- New deductions for 2025-2028. Several new temporary deductions address promises made during the presidential campaign, although not as directly as may have been expected. Importantly, income limits and phasedowns apply to many of these deductions, as well.

- Taxpayers aged 65+ now have a new deduction of $6,000 each. While the OBBBA does not exempt Social Security payments from tax, this new deduction gives a technically unrelated tax break to seniors that may temper the tax impact of that income.

- The bill provides new deductions for up to $25,000 of both tip and overtime income. Again, this is not an exemption of tip or overtime income from income tax, it is a deduction. Both tips and overtime still need to be reported as income and will be subject to FICA tax. Both deductions are subject to a number of requirements, and the deduction for overtime only includes the amount of overtime pay that is at a rate higher than the employee’s base wage rate.

- Finally, there is a new deduction of up to $10,000 of interest on a loan on a new vehicle purchased for personal use and manufactured in the U.S.

- Charitable giving rules. Beginning in 2026, charitable giving by non-itemizers (taxpayers taking the standard deduction) will be rewarded by a $1,000 ($2,000 for joint filers) deduction for cash gifts to public charities. But for large gifts to charity that would currently be eligible for itemization, OBBBA introduces a 0.5% of AGI floor for deductibility. This restricts allowance only to the extent charitable giving exceeds 0.5% of the donor’s AGI.

- ACTIONABLE ITEM: To get ahead of this change, donors may want to consider whether their circumstances justify accelerating some future giving into 2025 through bunching or contributing to a Donor-Advised Fund (DAF).

- Qualified Opportunity Zones. The Qualified Opportunity Zone program has been reinstated with fresh rounds of investment beginning anew in 2027. In the meantime, existing QOZ investors will be required to recognize gains at the end of 2026. It does not appear that there will be an option to roll those gains over into new QOZ investments, although there is still time for clarification as 2027 program parameters are yet to be finalized.

- QBI deduction for pass-through businesses. The QBI deduction for taxpayers actively engaged in small business activity was preserved with little change, giving business owners certainty after recent concerns that it might be eliminated or reduced. Effective 2026, the law adds a new minimum deduction of $400 for those with active qualified business income of at least $1,000.

- Trump accounts. OBBBA creates a new opportunity to put aside money for children who are under age eight (8) at the time the account is created. The goal is to supplement planning for certain life milestones (e.g., college or retirement). While details are still fluid, some highlights include:

- In the years before a child reaches 17, parents can contribute up to $5,000 per year. While these contributions are not deductible, funds in the account will grow tax-free until distribution.

- All babies born between 2025-2028 who have a Social Security number will be eligible to receive a federal government deposit of $1,000 into their account.

- All funds must be invested in a specific type of mutual fund, comprised primarily of U.S. equities.

- No distribution is permitted until the year the child turns 18, after which distributions are allowed without income tax and penalty if utilized for “qualified expenses”, including, among other things, post-secondary education and/or the purchase of a new home (up to $10,000). Funds, net of after-tax contributions, withdrawn for purposes other than “qualified expenses” prior to age 59 ½, will be subject to ordinary income tax and penalties (similar to an IRA).

While not a comprehensive description of the tax provisions of OBBBA, let alone other aspects of the bill, we hope that it has touched on issues most likely to be of interest to our clients. We are happy to answer any questions you may have on the contents of this message or on other aspects of OBBBA as clearer details emerge. One thing is certain; there will be a lot for all of us to learn in the coming months!

Elizabeth Hefferon